Global TV Market Reversal: Geopolitics and Soaring Costs This sharp correction is explained by an accumulation of macroeconomic factors stifling the supply chain. Persistent geopolitical tensions in the Middle East have led, as you know, to a rise in oil prices, directly impacting raw material and freight costs. Added to this are soaring memory component prices and new customs pressures. As Ricky Park, Senior Analyst at Omdia, explains: “The display industry is going through a real storm.” Manufacturers are forced to reconsider their pricing strategies, which has led us to significantly downgrade our demand outlook. TV Market: The End of Cost Absorption. On the television side, demand for panels for 2026 is expected to decline by 2% year-on-year. While manufacturers (particularly Chinese ones) were able to secure significant volumes of screens at historically low prices by the end of 2025 to flood shelves during the first quarter, this window of opportunity is now closed. Faced with the continued surge in production costs, the price shield artificially maintained by North American retailers is coming to an end: manufacturers are preparing to raise retail prices for the rest of the year, at the risk of seeing consumer demand and their market share erode. Laptops: Massive Freeze on Advance Purchases. The situation is even more critical in the laptop market. Unable to absorb component inflation, PC brands have already begun raising their prices by 20% to 30% since the second quarter of 2026. As an immediate consequence, the consulting firm Omdia has reduced its forecasts for this sector by 7.2 million panels, anticipating a massive freeze on replacement purchases by consumers in the second half of the year. For the end of the year, inventory management and the balance between profitability and attractiveness are therefore looking extremely precarious for the entire electronics industry.

Global TV Market Reversal: Geopolitics and Soaring Costs This sharp correction is explained by an accumulation of macroeconomic factors stifling the supply chain. Persistent geopolitical tensions in the Middle East have led, as you know, to a rise in oil prices, directly impacting raw material and freight costs. Added to this are soaring memory component prices and new customs pressures. As Ricky Park, Senior Analyst at Omdia, explains: “The display industry is going through a real storm.” Manufacturers are forced to reconsider their pricing strategies, which has led us to significantly downgrade our demand outlook. TV Market: The End of Cost Absorption. On the television side, demand for panels for 2026 is expected to decline by 2% year-on-year. While manufacturers (particularly Chinese ones) were able to secure significant volumes of screens at historically low prices by the end of 2025 to flood shelves during the first quarter, this window of opportunity is now closed. Faced with the continued surge in production costs, the price shield artificially maintained by North American retailers is coming to an end: manufacturers are preparing to raise retail prices for the rest of the year, at the risk of seeing consumer demand and their market share erode. Laptops: Massive Freeze on Advance Purchases. The situation is even more critical in the laptop market. Unable to absorb component inflation, PC brands have already begun raising their prices by 20% to 30% since the second quarter of 2026. As an immediate consequence, the consulting firm Omdia has reduced its forecasts for this sector by 7.2 million panels, anticipating a massive freeze on replacement purchases by consumers in the second half of the year. For the end of the year, inventory management and the balance between profitability and attractiveness are therefore looking extremely precarious for the entire electronics industry. Home Theatre

Global TV Market: After the euphoria of the first quarter, bleak forecasts for 2026

16.06.2026 • 11h29

The analysis firm Omdia paints an alarming picture of the global display market for the whole of 2026. In stark contrast to the upturn in the first quarter driven by the World Cup effect, the new forecasts anticipate a sharp drop in demand, weighed down by component inflation and a tense geopolitical context that will force manufacturers to raise their selling prices in the coming months.

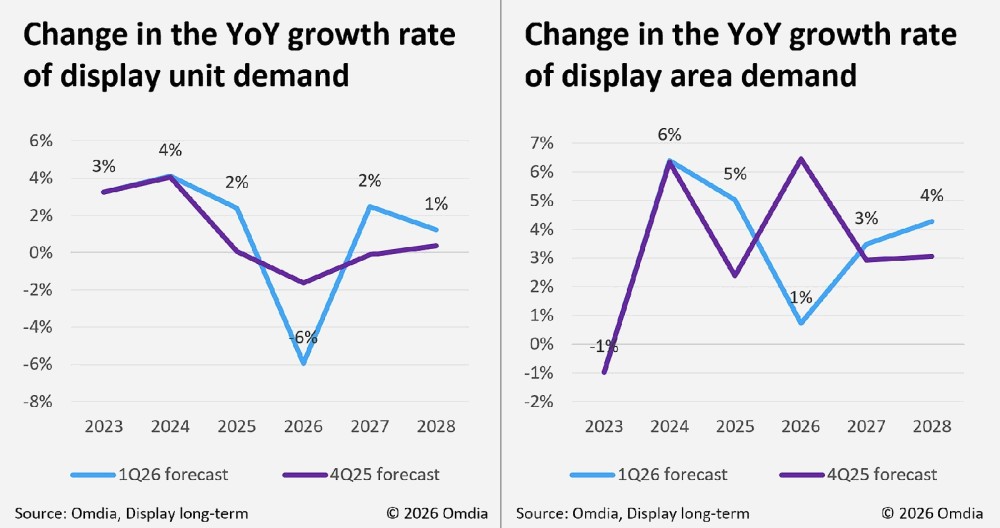

Just yesterday, the figures suggested a positive trend, with global TV shipments up 6% in the first quarter of 2026, boosted by stockpiling by distributors ahead of the major football event (see our Omdia news item: global TV market to grow by 6% in the first quarter of 2026 before the World Cup). But this appears to be a mirage. In its latest Display Long-Term Demand Forecast Tracker report, Omdia has drastically revised its forecasts downward for the entire year. Global demand for panels (across all media types) is now expected to decline by 6% in volume year-on-year, a major deterioration compared to the initially anticipated 2% drop. Meanwhile, display area growth has collapsed to a meager +1%, compared to the +6% expected just a few months ago. Global TV Market Reversal: Geopolitics and Soaring Costs This sharp correction is explained by an accumulation of macroeconomic factors stifling the supply chain. Persistent geopolitical tensions in the Middle East have led, as you know, to a rise in oil prices, directly impacting raw material and freight costs. Added to this are soaring memory component prices and new customs pressures. As Ricky Park, Senior Analyst at Omdia, explains: “The display industry is going through a real storm.” Manufacturers are forced to reconsider their pricing strategies, which has led us to significantly downgrade our demand outlook. TV Market: The End of Cost Absorption. On the television side, demand for panels for 2026 is expected to decline by 2% year-on-year. While manufacturers (particularly Chinese ones) were able to secure significant volumes of screens at historically low prices by the end of 2025 to flood shelves during the first quarter, this window of opportunity is now closed. Faced with the continued surge in production costs, the price shield artificially maintained by North American retailers is coming to an end: manufacturers are preparing to raise retail prices for the rest of the year, at the risk of seeing consumer demand and their market share erode. Laptops: Massive Freeze on Advance Purchases. The situation is even more critical in the laptop market. Unable to absorb component inflation, PC brands have already begun raising their prices by 20% to 30% since the second quarter of 2026. As an immediate consequence, the consulting firm Omdia has reduced its forecasts for this sector by 7.2 million panels, anticipating a massive freeze on replacement purchases by consumers in the second half of the year. For the end of the year, inventory management and the balance between profitability and attractiveness are therefore looking extremely precarious for the entire electronics industry.

Global TV Market Reversal: Geopolitics and Soaring Costs This sharp correction is explained by an accumulation of macroeconomic factors stifling the supply chain. Persistent geopolitical tensions in the Middle East have led, as you know, to a rise in oil prices, directly impacting raw material and freight costs. Added to this are soaring memory component prices and new customs pressures. As Ricky Park, Senior Analyst at Omdia, explains: “The display industry is going through a real storm.” Manufacturers are forced to reconsider their pricing strategies, which has led us to significantly downgrade our demand outlook. TV Market: The End of Cost Absorption. On the television side, demand for panels for 2026 is expected to decline by 2% year-on-year. While manufacturers (particularly Chinese ones) were able to secure significant volumes of screens at historically low prices by the end of 2025 to flood shelves during the first quarter, this window of opportunity is now closed. Faced with the continued surge in production costs, the price shield artificially maintained by North American retailers is coming to an end: manufacturers are preparing to raise retail prices for the rest of the year, at the risk of seeing consumer demand and their market share erode. Laptops: Massive Freeze on Advance Purchases. The situation is even more critical in the laptop market. Unable to absorb component inflation, PC brands have already begun raising their prices by 20% to 30% since the second quarter of 2026. As an immediate consequence, the consulting firm Omdia has reduced its forecasts for this sector by 7.2 million panels, anticipating a massive freeze on replacement purchases by consumers in the second half of the year. For the end of the year, inventory management and the balance between profitability and attractiveness are therefore looking extremely precarious for the entire electronics industry.